Tokenization: When Ownership Becomes Programmable

On my weekly AI-Macro-Crypto YouTube show, the podcast I have referenced the most about the impact of AI on our lives and investments has been Moonshots with Peter Diamandis. Last year, I remember driving in Maine, looking out over the ocean on a beautiful sunny summer day, and listening to an episode titled Tech Experts Break Down the Incoming AI-Crypto Collision That Will Redefine Global Power. At the time, AI was still considered a bubble in the minds of most institutional investors, and crypto was still largely misunderstood. But as I listened, I knew I would eventually come back to that conversation when investors were forced to accept that AI and crypto were not separate stories. They were two parts of the same coming financial and technological transition.

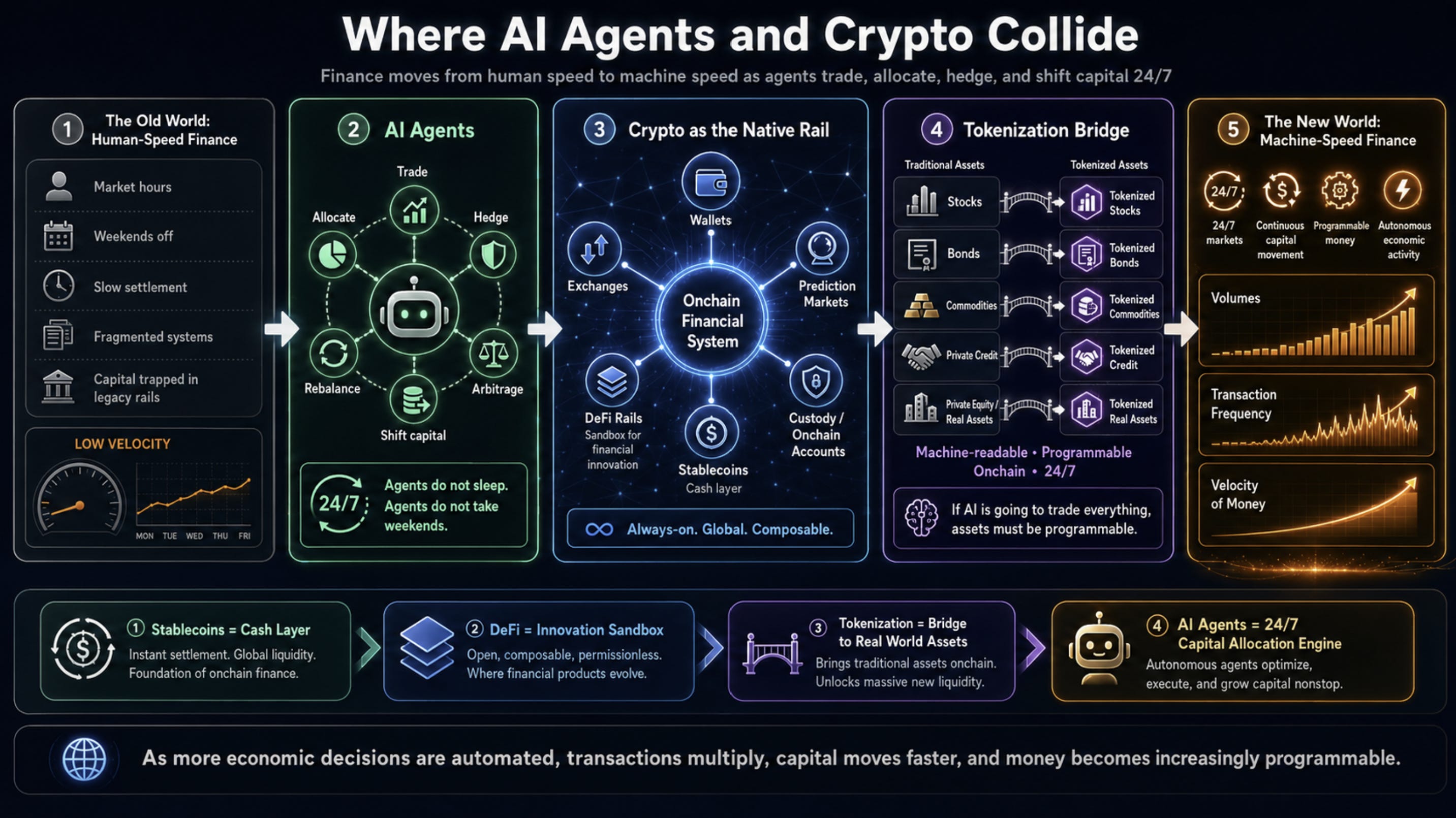

That belief was built around the one thing I thought would change investors’ doubts about AI: agents. AI agents speed up adoption because they move AI from a tool that answers questions to a system that takes actions. They also help answer the “where are the revenues?” question by turning intelligence into workflows, automation, software development, trading tools, business processes, and eventually economic activity. 2026 has brought the rise of AI agents, both as a driver of market alpha and as a source of pressure on software and other long-duration assets. Agents increase demand for tokens, compute, and real-time coordination, but they also create uncertainty around the terminal value of traditional SaaS. Investors are currently focused on semiconductors, optical fiber, data centers, and hardware, but many of those are cyclical areas of the AI buildout. Unlike SaaS, which grew steadily and tied to payrolls along with nominal GDP, the capex buildout of AI will be subject to cycles around shortages, bottlenecks, input inflation, and margin compression. As wealth managers, pensions, and long-term investors again look for technology growth that is not disrupted by AI and does not require ever-rising capex intensity, the crypto guardrails become much more important. The AI-crypto collision is no longer theoretical. It is here now.

As one guest on the Moonshots podcast put it when discussing the GENIUS Act last year, it may be “the most significant economic legislation and changes that we’ve seen in our lifetimes.” He went even further, calling it “as big a shift in our economy as I think we’ve ever seen.” What made the moment so important was not simply crypto itself, but the creation of legal guardrails around stablecoins, tokenization, and digital assets. In other words, the United States is beginning to build the new financial rails for an AI-driven, internet-native economy, one where, as the podcast said, “When we give our AI agents access to that, we’re going to see an explosion in the economy.”

This discussion was not about meme coins, speculation, or another trading cycle. It was about the economic guardrails of the global system beginning to change and go digital to serve digital agents. One of the most important lines in the conversation was that we are moving into an age where you cannot rely on the Swift network, three-day settlement, and high transaction costs in a world being accelerated by AI. The podcast’s deeper point was that AI and crypto are not separate stories. AI increases the need for faster coordination, faster settlement, faster capital allocation, and programmable systems. Crypto provides the rails. Stablecoins become programmable money. Tokenization becomes programmable ownership. AI agents become the future users of both. That was the theory. The recent DoorDash stablecoin news and the acceleration of tokenization are the evidence that this theory is now moving from podcast conversation to market structure.

That is why this paper is the follow-up to my last piece on programmable money. In that piece, I wrote about why the DoorDash stablecoin news mattered more than it first appeared. The point was not simply that another company was exploring faster payouts. The point was that money itself was beginning to behave differently. In the DoorDash example, stablecoins showed how money can be distributed, routed, and managed at the moment it is created. A customer pays, and that payment can be split instantly between the platform, the driver, and the merchant. No batching. No unnecessary delay. No separate reconciliation process after the fact. That was the first step in the evolution of the crypto financial guardrails: money becoming programmable. Tokenization is the next step because it applies the same logic to ownership. Assets, shares, funds, collateral, private investments, and eventually entire portfolios can begin to move with the same software-driven logic. Stablecoins change how money moves. Tokenization changes how ownership moves. When those two forces combine, the financial system starts to become programmable.

The important part is that this progress is happening while many investors are still waiting for “clarity” from Washington and while crypto sentiment remains subdued. The conversation remains focused on the slow movement of the CLARITY Act and the still-uncertain regulatory path for crypto market structure. But the infrastructure is not waiting. Stablecoins now have more than $272 billion in global circulating supply and $10.2 trillion in adjusted transaction volume over the last 12 months, according to Visa’s on-chain analytics. Nasdaq received SEC approval to allow certain securities to trade and settle in tokenized form, initially focused on Russell 1000 companies and ETFs tied to major benchmarks like the S&P 500 and Nasdaq 100. Bullish announced a $4.2 billion acquisition of Equiniti, a major transfer agent serving more than 20 million shareholders and processing roughly $500 billion in annual payments. Securitize partnered with Computershare, which services more than 25,000 companies and 58% of the S&P 500, to help U.S. companies issue tokenized shares while preserving dividends and proxy voting. These are not isolated headlines. They are the plumbing phase of a new financial network, and it is happening now.

The venture capital market is starting to confirm the same message. Andreessen Horowitz’s crypto arm recently raised $2.2 billion for its fifth dedicated crypto fund, even though the industry is still recovering from the excesses of the last cycle. The important part is not just the size of the fund. It is the focus. The firm highlighted stablecoins, tokenization, perpetual futures, prediction markets, and AI agents as some of crypto’s most promising areas for investment. That list matters because it is not built around the old Web3 hype cycle. It is built around financial infrastructure, market structure, and software-driven coordination. Stablecoins are becoming the money layer. Tokenization is becoming the ownership layer. Prediction markets and perpetual futures are becoming new venues for price discovery. AI agents may become the future users of these programmable rails. The Moonshots podcast warned that the combination of AI and crypto could accelerate the economy in ways most people still do not understand. The capital now being raised around these same themes suggests serious investors are beginning to position for that possibility.

This is why tokenization matters so much. Tokenization is the process of representing ownership of an asset as a digital token on a blockchain or distributed ledger. That asset can be a Treasury bill, a money market fund, an ETF, a share of stock, a private company interest, a real estate claim, a private credit instrument, or eventually almost anything that can be legally represented, verified, transferred, and settled. At first glance, that may sound like a technology upgrade. In reality, it is a market-structure upgrade. The financial system looks instantaneous from the outside, but inside the machine it is still full of settlement cycles, custodians, transfer agents, clearinghouses, fund administrators, reconciliation systems, market hours, batch processing, and legal recordkeeping. Tokenization attacks those delays. It turns ownership into something that can be programmed, transferred, settled, collateralized, and integrated with software. The Moonshots discussion used a simple real estate example: if ownership can be verified instantly and represented digitally, then dormant value can become collateral faster, ownership can become fractional, and assets can become usable in ways the old system made difficult. That is the shift. It is not just faster trading. It is a new relationship between ownership, liquidity, and collateral.

But the deeper story has always been larger than faster settlement or fractional ownership. The real story is the eventual merging of two financial universes: roughly $800 trillion of traditional financial assets and roughly $3 trillion of crypto assets that have been living on separate rails. Tokenization is not just the bridge between those worlds. It is the Trojan horse. It allows traditional assets to move onto crypto rails without forcing investors to think they are leaving the regulated financial system behind.

This is also where tokenized ETFs may become one of the most important bridges. The ETF was already one of the great financial innovations of the last 30 years because it turned a basket of securities into a liquid, tradable product. Tokenization can take that idea further. A traditional ETF is a basket. A tokenized ETF can become a programmable portfolio container. That container could eventually hold public equities, tokenized Treasuries, stablecoins, crypto tokens, private credit, private company interests, real estate, infrastructure assets, and other real-world assets. In the old system, these lived in separate markets with separate custodians, separate settlement systems, separate access points, and separate investor bases. In the tokenized system, they can increasingly become components of the same programmable portfolio. This is how crypto tokens, public companies, and private companies begin to merge. Crypto moves into regulated investment wrappers. Public companies can exist as traditional shares and tokenized shares with the same legal rights. Private company ownership can gradually become more standardized, fractionalized, transferable, and usable inside broader investment products. The public market becomes more programmable. The private market becomes more accessible. The ETF becomes the bridge between the two.

That is the wake-up call for investors. The mistake is to think of crypto only in terms of bull markets, bear markets, halving cycles, liquidity cycles, and token prices. The more important story is the infrastructure buildout happening underneath the surface. Stablecoins are becoming programmable cash. Tokenized Treasuries can become programmable collateral. Tokenized ETFs can become programmable portfolios. AI agents will become the active users of these rails because they cannot operate inside a legacy financial system built around batching, settlement delays, and manual reconciliation. We have seen this adoption curve before. Think back to the years just before the App Store and the rollout of mobile broadband. The plumbing had to be laid before the platform and social media eras could explode. We are in that same infrastructure phase today. But this time, the rails are connecting a new economy where the consumer is both human and digital. AI agents will be the catalyst that ignites the network effects across this system. The same dynamic we are already seeing in AI token usage could eventually show up in crypto transaction volumes. As agents move from answering questions to taking actions, they will create more transactions, more settlement events, more collateral movements, more portfolio rebalances, and more automated payments. In other words, the velocity of money can rise because software agents do not operate on human time. They operate continuously. If agent usage is already producing parabolic-looking charts in tokens consumed, compute demand, and semiconductor-related revenues, then programmable money and tokenized assets could produce similar parabolic pressure on financial volumes as agents begin to transact. This is not only an upside story for digital assets. It is a severe margin-compression threat to any financial business model that depends on friction, float, restricted access, or unnecessary delay.

That is why the AI-crypto collision matters even more now than it did when I first listened to that Moonshots episode. This year has become the year of AI agents. The conversation has moved from chatbots answering questions to agents taking actions, writing code, managing workflows, searching across systems, and beginning to operate as digital workers. Once agents start interacting with money, portfolios, collateral, payments, and ownership, the need for programmable financial rails becomes much more urgent. AI agents cannot fully operate in a financial system built for banking hours, settlement windows, and manual reconciliation. They need programmable money and programmable ownership. Even JPMorgan, led by Jamie Dimon, one of the most outspoken critics of Bitcoin and crypto over the years, is now showing how seriously it takes tokenization. The firm has argued that tokenization will help reshape ETFs and the broader funds industry, and it is already running tokenized ETF proof-of-concepts through Kinexys. That is the signal. The train is leaving the station. The Moonshots conversation called this a Pandora’s box of innovation. That is the right framing. The box is opening while sentiment is still subdued. Investors waiting for perfect clarity may miss the fact that the new financial guardrails are already being built. This is not a world where crypto replaces everything. It is a world where crypto rails are absorbed into everything. That is the next network effect. And it is already beginning.

Excellent piece Jordi. Scarcity, Function, and True Efficiency. As Elon said, the future won't use dollars, just massive energy. As Tom Lee said, crypto is monetizing the value of massive energy. $MSTR $BMNR

Excellent piece, Jordi. I’ve been writing about the same underlying shift — programmable money evolving into programmable ownership — and how AI agents will be the primary users of these new rails. In my latest article, "Crypto AI M&A: The Alpha Compound", I explore how this collision is already driving real M&A activity and creating compounding advantages. Your breakdown of tokenization as the bridge between TradFi and crypto infrastructure felt like the perfect complement.

Appreciate the clarity.